®®

®®Understanding Auto Finance Loan Approval Process

|

AUTOMOTIVE UNDERWRITING 101

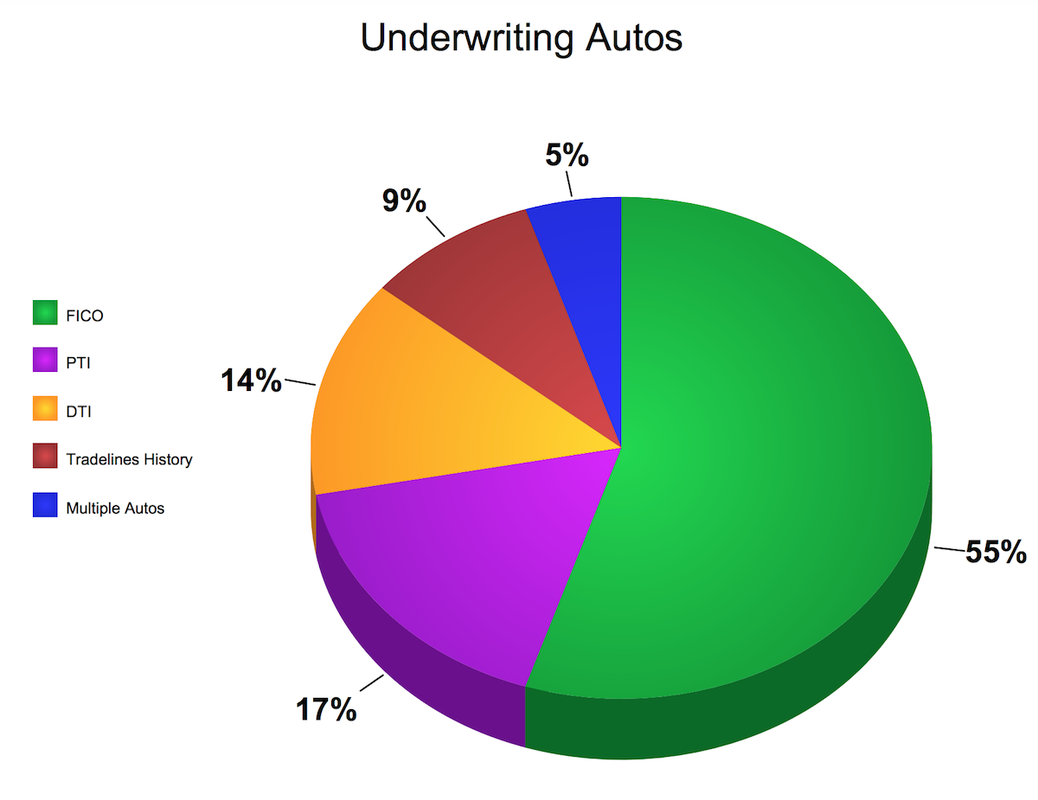

What factors are reviewed to approve my car payment? LTV limit 130% Loan to Value (LTV) is the comparison of the amount borrowed to the invoice value of the vehicle. LTV ratios up to 130% are allowable for consumers who want to finance accessories or roll negative trade-in equity into the loan approval. Lower LTV ratios, below 90%, often trigger interest rate discounts. DTI limit 45%

Debt to Income (DTI) is the amount of monthly bills on the buyer’s credit bureau combined with monthly housing cost divided by gross monthly income before income tax deductions. High debt ratios trigger secondary audits of credit files and/or a lender interview prior to a decision. If a buyer has outgoing bills of $2500, and makes $3000 monthly income, then the underwriter will not approve a loan with a $600 car payment. PTI limit 15% Payment to Income is the monthly car payment divided by the applicant’s monthly income. Standard underwriting guidelines from auto lenders allow 15% of your monthly income to be spent on your car note. If you earn $3000 per month, then you can afford a $450 car payment at 15% PTI. Lenders can make exceptions up to 5% in this category if other factors are favorable enough. See car payments by salary for more PTI calculations. Number of open auto loans Consumers with one open auto are at lower risk of default. If a consumer has an open auto loan, but trades it in, then the risk remains singular. If not trading, then risk of default increases. Think about it from a practical perspective. We all need one vehicle to get to work. But do we need the second vehicle? If finances get tight, it’s much easier to let the second car go, because the first car will still be around.

Cash Down

The applicant’s out-of-pocket start payment should cover government fees and reduce the amount financed enough to keep payment-to-income ratios in line. Zero down is suitable for well qualified buyers, but 10% minimum should be requested on B Tier and below. Employment history Length of employment is a repayment risk factor. Short and sporadic employment increases the risk of default and/or late payments. Two years or more at the current position alleviates risk in this pricing factor. Proof of income should be requested via pay stub (dated within 30 days) prior to loan approval for applications with high DTI, high PTI, or short term employment. Residence history The address on the application should appear somewhere in the applicant's credit bureau. Inability to pinpoint the location of the collateral is a risk factor. This flag is alleviated by proof of address via recurring utility bill. Number, length, and level of prior credit tradelines The number of credit cards and installment loans on an applicant’s credit bureau, the highest amount borrowed and repaid, and the time since inception of accounts is a solid indication of future performance. If a buyer has a 700 FICO score but only three prior tradelines with a high of $3000, then an auto loan of $80,000 would be out of range. Buyers with seasoned accounts on file are lower risk than buyers with new accounts. There's an adjustment period as new debt settles into the monthly budget. Default risk is higher during the adjustment period. |

|

Tradeline balance-to-limit ratios The utilized credit amount divided by available credit equals the balance-to-limit ratio. Buyers are at higher risk if current accounts are maxed out. Available credit is a safeguard during tight-budget months. Buyers often close credit accounts when debt is paid, however paid accounts should be left open when possible to keep balance-to-limit ratios in the most favorable position, and to maintain the credit history on file. Auto payment history Review the length and quality of prior similar credit tradelines. If other loans are shaky, but auto history is solid, then risk of auto default is low. Many consumers will make their car note even if other bills fall behind. How many 30, 60, or 90 day late car payments are on file? The risk assessment should focus on the type of collateral borrowed in particular, and not weigh heavily on other tradelines if the consumer has shown a commitment in this manner. Collateral consideration Vehicle age, condition (new or used), usage (private vs commercial), and odometer reading must be factored into the decision. Older vehicles pose a higher risk than newer vehicles because repair bills can affect monthly budget unexpectedly. Commercial autos are at higher risk because they are driven more miles and given more abuse, causing them to depreciate in value quicker, thus becoming less favorable as collateral in the long run.

FICO Experian Auto is the preferred credit score for vehicle underwriting. In particular, score-driven banks use Experian Auto 8 to determine interest rates. Lenders have different scoring models depending on acquisition goals and market strategies. Credit unions set the interest rate primarily from your FICO score. Other lenders start with the score, but have interest rate adds and deductions depending on LTV, DTI, and PTI ratios. See the credit score calculator for car payments based on FICO. Loan amount The amount borrowed should be capped at the amount that fits within the applicant’s budget relative to PTI, DTI, and LTV based on the interest rate calculated from the FICO score using the in-house rate sheet below. |

Rate Sheet

|

|

EXPLANATION OF LOAN ELEMENTS

Sale Price Price after dealer discount but before factory rebate is applied. APR: Interest Rate Annual Percentage Rate (APR) is determined primarily from the buyer’s credit score, but also dependent upon income and debt. APR increases as the loan term increases. For example, a well-qualified buyer may receive an approval for $65,000 at 4.39 for 60 months, 5.39 for 72 months, or 6.49 for 84 months. But a first-time buyer may be capped at $11,000 for 60 months at 14.99%. See APR Loan Math to understand how interest is calculated. Term

Loan length is sometimes disclosed in years, but is always converted to months on the purchase contract. The most common term is 72 months. Other common terms are 24,36,48,60,84, and sometimes 96 months. Terms longer than 72 months usually require at least $25,000 amount financed. Down Payment Simple, right? It’s your cash down. But keep in mind that your trade-in equity and factory rebate are on separate lines in the contract. The down payment line is just for out-of-pocket cash, credit card, or check. This amount is usually around 10% of the sale price, or enough to cover the tax, license, and registration. The down payment is negotiable so agree on an amount that comfortably brings the monthly payment into your planned range. |

Manufacturer’s Rebate

This is a factory discount - not costing the dealer anything - that is applied toward the purchase to reduce the total cost. For taxation, it's technically a cash-back promotion from the manufacturer that buyers can use toward the down payment on a new vehicle. Amount Financed The remaining balance after all credits and additions have been applied is the amount financed. Abbreviated ATF by lenders who require minimum limits for different loan terms as follows: Minimum ATF for 60 Months - $10,000 | 72 months - $15,000 | 84 months - $25,000 | 96 months - $30,000. Net Price After Rebate The sale price minus the rebate, before taxes and fees are included, is disclosed as the net price. This is what you tell your friends you bought the car for. Trade Difference A trade-in vehicle can bring positive or negative equity to a deal depending on the value compared to the loan payoff balance. This trade difference will either decrease or increase the total amount financed. If your car is worth 2000 and the payoff is 3000 then the new car loan will be 1000 higher than if you had no trade-in. Total Expense Informational disclosure aimed at disclosing the total transaction cost after all fees including tax, license, registration, and finance charges are added to the net price. Finance Charge The total interest paid to the bank by the end of the loan if all payments are made without early payoff is disclosed as the Finance Charge. |

|

|

CAR LOAN FAQ

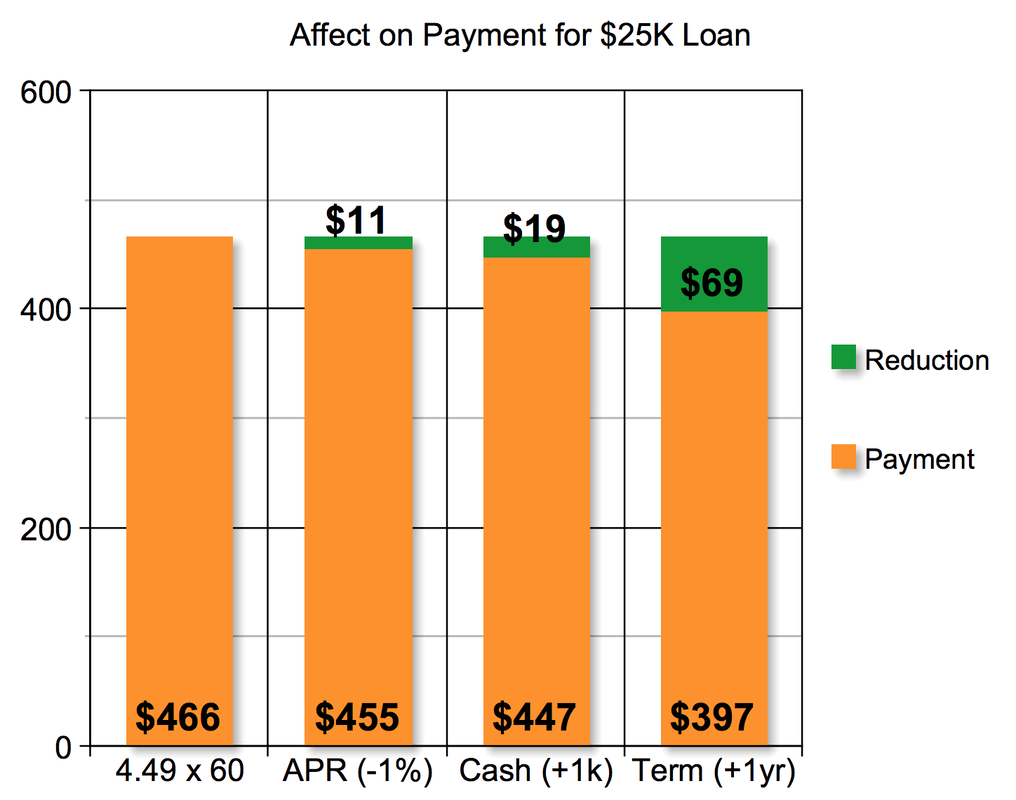

Am I taxed on rebate? What about trade-in? Some states in the USA charge tax after rebate and trade-in, some charge on one but not the other, and some charge on the full sale price without credit for either. Do I need a down payment to buy a car? No. Down payments are not required by auto lenders and it has become increasingly common to finance 100% with zero out-of-pocket. How much money can I borrow? You can borrow $9000 for every $1000 of your monthly income if all other budget factors are in line. If you earn $4000 per month, then you can borrow $36,000 with a monthly payment of $600. How can I make my monthly payment lower? After you agree on sale price, rebate, and trade-in value, you can still lower your monthly payment by increasing cash down or by selecting a longer term. What reduces my monthly car payment the most?

The length of the loan term affects payment more than any other factor.

How much does loan term affect payment?

A three-year loan payment is nearly double a six-year loan. Is there a penalty for early payoff during a car loan? No. You may payoff the remaining principal at any time without paying the remaining interest. Will I save money by paying off my car loan early? Yes. Auto finance charges are billed on a monthly basis, not due as a lump sum at any time, and therefore each month of early payoff is a month of interest saved. How much does my down payment affect my monthly payment? Every $1000 of down payment reduces $20 of monthly payment approximately. How are car loans approved so fast? On paper, collateral value is the reason car loans are quick and easy with low interest rates and high loan amounts compared to unsecured loans; because banks can quickly get their money back by repossession of collateral. However, in the real world, repo of collateral is more of a deterrent to alert future buyers than it is a recovery of current funds. The reason auto loans are so lucrative for banks is because consumers will pay when the threat of losing their ride comes into play. Consumers will let other debts default before losing their cars. |

Auto Loan Calculators

Ad